Home Warranty vs. Home Insurance: Key Differences

House Escort Team

Home Warranty vs. Home Insurance: Key Differences

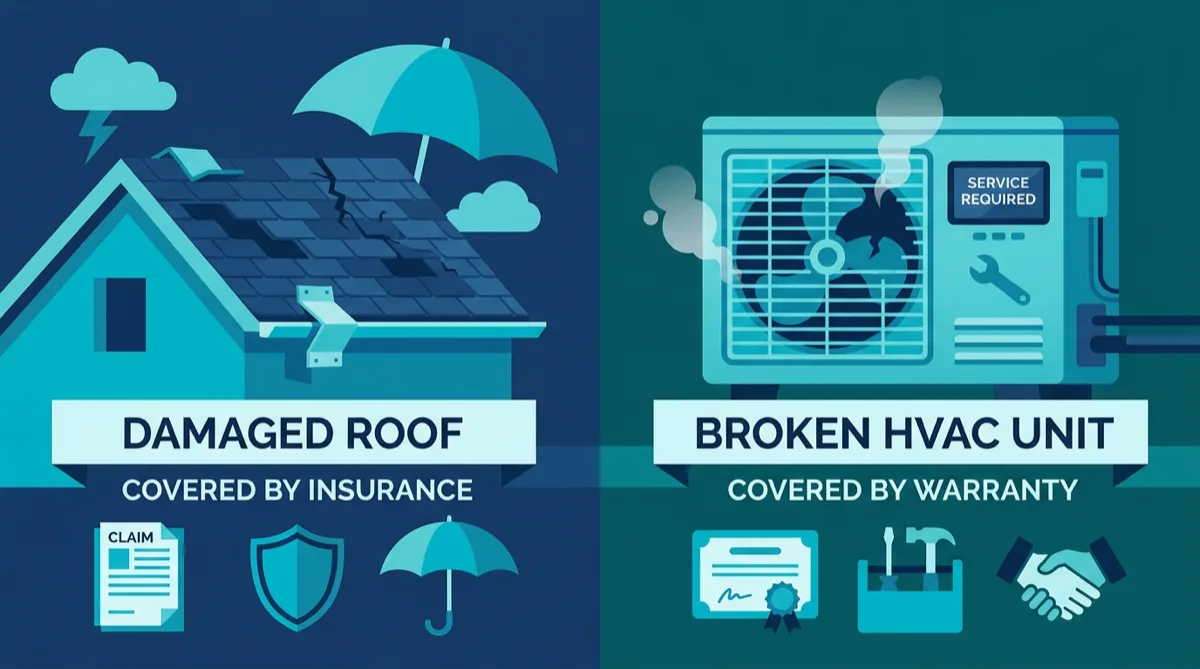

When something breaks in your house — a refrigerator dies, a pipe bursts, the roof leaks after a storm — the first question most homeowners ask is: “Is this covered?”

The answer depends on which product you’re asking about, and many homeowners discover the hard way that their home warranty doesn’t cover the storm damage, and their home insurance doesn’t cover the appliance failure.

This guide explains the difference between home warranty vs. home insurance, what each covers, and how to decide if both are worth the cost in Texas.

What Is Home Insurance?

Homeowners insurance (also called hazard insurance) is a policy that protects your home and belongings from sudden, unexpected damage caused by external events.

It is:

- Required by most mortgage lenders

- Event-based — covers damage from specific named perils

- Not optional for most homeowners with a mortgage

Standard homeowners insurance typically covers:

- Fire, smoke, and lightning damage

- Windstorm and hail damage (key in Texas — hail is a frequent and expensive claim)

- Theft and vandalism

- Water damage from burst pipes (sudden and accidental — not gradual leaks)

- Falling objects (trees, aircraft)

- Liability if someone is injured on your property

What standard policies typically do NOT cover:

- Flooding (requires a separate NFIP or private flood policy — critical for Houston-area homeowners)

- Earthquake (separate rider)

- Normal wear and tear

- Appliance or system mechanical failure

- Neglect or deferred maintenance

In Texas, review your policy carefully for windstorm coverage. HO-3 policies (the most common form) cover windstorm, but some Gulf Coast properties require separate windstorm coverage through the Texas Windstorm Insurance Association (TWIA).

What Is a Home Warranty?

A home warranty is a service contract — not an insurance policy — that covers the repair or replacement of home systems and appliances that fail from normal wear and tear.

It is:

- Optional — no lender requires it

- Mechanical failure-based — covers breakdowns, not damage events

- Typically renewable annually at the homeowner’s discretion

Standard home warranty typically covers:

- HVAC systems (heating and cooling)

- Plumbing systems and stoppages

- Electrical systems

- Appliances: refrigerator, dishwasher, range, microwave, washer/dryer (depending on plan)

- Water heater

What home warranties typically do NOT cover:

- Pre-existing conditions (most providers exclude known or detectable issues at purchase)

- Code violations

- Secondary damage caused by a failed system (e.g., water damage from a leaking appliance)

- Damage from improper installation or maintenance

- Cosmetic defects

The fine print: Home warranty claims are more often denied than homeowners expect. Providers may cite pre-existing conditions, improper installation, or lack of maintenance records. Read the exclusions before purchasing.

Side-by-Side Comparison

| Feature | Home Insurance | Home Warranty |

|---|---|---|

| Required by lenders | ✓ | |

| Covers weather damage | ✓ | |

| Covers appliance breakdown | ✓ | |

| Covers wear and tear | ✓ | |

| Covers flooding | Rider only | |

| Covers theft/liability | ✓ | |

| Annual cost (Texas) | $1,500–$4,000+ | $400–$900 |

| Deductible/service fee per claim | $500–$2,000 | $75–$125 |

Home Insurance Costs in Texas

Texas is one of the most expensive states for homeowners insurance in the country — primarily because of hail, wind, and storm risk. Average annual premiums in Texas:

- Houston area: $2,500–$5,000+ (storm and flood risk)

- Dallas/Fort Worth: $2,000–$4,000

- San Antonio: $1,800–$3,500

- Austin: $1,800–$3,200

These are broad ranges. Your actual premium depends on home value, construction type, distance to coast, claims history, and deductible choice.

Note: Most Texas homeowners insurance policies have a separate, higher deductible for wind and hail claims — often 1–2% of the home’s insured value rather than the standard flat deductible. On a $400,000 home, that’s a $4,000–$8,000 deductible for hail damage.

Home Warranty Costs in Texas

Home warranty plans in Texas typically run $400–$900/year depending on coverage level:

- Systems-only plan: $400–$600/year — HVAC, plumbing, electrical, water heater

- Appliances-only plan: $350–$500/year — refrigerator, dishwasher, washer/dryer, range

- Comprehensive plan: $600–$900/year — systems + appliances

Most plans also charge a service call fee ($75–$125) per claim.

Popular providers in Texas: American Home Shield, Choice Home Warranty, First American Home Warranty, Cinch Home Services. Compare coverage terms carefully — the brand matters less than the specific contract exclusions.

Is a Home Warranty Worth It in Texas?

The math is straightforward in theory: if your expected repair costs exceed the warranty cost + service fees, it’s worth it. In practice, it depends on:

Age of your systems and appliances. A home warranty is most valuable when systems and appliances are 5–15 years old — old enough to be prone to failure, but not so old that warranty companies decline coverage.

Your financial buffer. If an AC failure in July (a $5,000–$12,000 replacement) would create genuine financial hardship, the warranty provides peace of mind worth the annual cost. If you have a strong emergency fund and your systems are newer, self-insuring may be smarter.

Texas-specific: HVAC. In Texas, HVAC failure is the most expensive single system failure a homeowner faces. A policy that covers the full replacement of a central AC system (after a service fee) can pay for several years of warranty costs in one claim. This is the primary reason Texas homeowners buy home warranties.

When Both Products Work Together

Home insurance and home warranty cover fundamentally different risks — they don’t overlap significantly. A hail storm damages your roof → home insurance. Your AC compressor fails from age → home warranty. Both scenarios happen frequently in Texas; both products have a logical place.

For homeowners in older homes (10+ years) with aging systems, carrying both is a reasonable risk management strategy. For homeowners in newer homes with builder warranties still active, the home warranty value is lower.

For reliable HVAC contractors, plumbers, and electricians when your warranty claim is denied or you need faster service than a warranty company dispatches, find vetted pros at houseescort.com — free for homeowners.

Frequently Asked Questions

Does home insurance cover a broken AC in Texas?

Standard homeowners insurance does not cover mechanical breakdown of your AC system from normal wear. It would cover AC equipment damaged by a covered event — fire, lightning, or a hailstorm that physically damages the outdoor condenser. For mechanical failure, a home warranty covers AC repairs and replacement.

Can I get a home warranty after a problem occurs?

Home warranties typically have a waiting period (30 days) before coverage activates, specifically to prevent homeowners from purchasing coverage for a known failing system. Pre-existing conditions at the time of policy purchase are generally excluded.

What does home insurance not cover in Texas that surprises people?

The most common surprises: flooding (requires separate flood policy), sewer or drain backup (requires a rider), wind/hail with a separate percentage deductible, and gradual water damage from slow leaks. Many Houston-area homeowners discover their flood damage isn’t covered by their standard homeowners policy.

Do I need a home warranty if my home is new?

New construction typically comes with a builder’s warranty — 1 year on workmanship, 2 years on systems, 10 years on structural defects (varies by builder). During the builder warranty period, a separate home warranty adds limited value. After it expires, reassess based on your home’s system ages.

How do I file a home warranty claim?

Contact your warranty provider directly (phone or online portal) and describe the problem. They’ll dispatch a contractor from their network — you pay the service fee, they pay the contractor. Important: don’t call your own contractor first for a warranty-covered issue, as unauthorized repairs are typically not reimbursable.